By Brian French | April 9, 2026

THE EVERYTHING MARKET: HOW TOKENIZATION IS ABOUT TO REWIRE GLOBAL FINANCE, KILL THE BOOKIE’S VIG, AND LET YOU OWN A PIECE OF THE MONA LISA

From Wall Street closing bells to 24/7 blockchain trading, from overpriced sportsbook juice to frictionless prediction markets, the tokenization revolution is coming for every asset class on earth — and the company quietly running the plumbing for all of it trades on the NYSE under the ticker CRCL.

Finance & Technology

Not long ago, the idea of buying a fractional stake in a Manhattan skyscraper, a Picasso painting, a thoroughbred racehorse, or a government bond — from your phone, at 2 a.m. on a Sunday, with instant settlement and no middleman taking a cut — would have sounded like the fever dream of a particularly optimistic fintech pitch deck. Today, it is not only possible. It is happening. And the financial world, from the trading floors of Wall Street to the sports betting apps on your lock screen, is about to change in ways that make the invention of the online brokerage account look like a minor software update.

The engine driving all of it is a single, deceptively simple idea: tokenization. The process of converting ownership rights in any asset — a building, a stock, a painting, a bond, a stadium seat, a racehorse, a bottle of 1982 Pétrus — into a digital token recorded immutably on a blockchain. Buy the token, own a provable, tradeable, legally enforceable piece of the underlying asset. No broker required. No banker required. No three-week settlement period required. And, increasingly, no closing bell required either.

But before any token can be traded, before any asset can be fractionalized, before any prediction can be settled or any building sold in fractional shares to ten thousand investors simultaneously, someone has to handle the money. Someone has to provide the digital dollar that makes the whole ecosystem function. And for that, the financial world has increasingly turned to one company: Circle Internet Group and its USDC stablecoin — the regulated digital dollar that has become, quietly and with very little fanfare from the mainstream press, the monetary backbone of the new financial system.

CIRCLE AND USDC: THE REGULATED DOLLAR AT THE CENTER OF EVERYTHING

If tokenization is the revolution, Circle is the central bank that makes it function. Founded in Boston in 2013 and now headquartered in New York, Circle Internet Group issues two types of stablecoin: USDC, pegged 1:1 to the U.S. dollar, and EURC, a euro-denominated stablecoin. It also issues USYC, a tokenized money market fund backed by U.S. Treasury holdings. The company went public on the New York Stock Exchange in June 2025 under the ticker CRCL.

The numbers behind USDC are, at this point, genuinely staggering. USDC in circulation reached $75.3 billion at year-end 2025, up 72% year over year, while quarterly on-chain transaction volume hit $11.9 trillion — a 247% increase. To put that in perspective: $11.9 trillion in quarterly volume is roughly half the annual GDP of the United States, flowing through a digital currency that most Americans have never heard of, settling in seconds, around the clock, every day of the year.

USDC is issued by regulated entities of Circle and presented as an internet-native, fully reserved digital dollar designed for near-real-time, low-cost global transactions. USDC is backed by the equivalent value of U.S. dollar-denominated assets, with the Circle Reserve Fund custodied at The Bank of New York Mellon and managed by BlackRock. That last detail deserves emphasis: the reserves backing the world’s leading regulated stablecoin are managed by the world’s largest asset manager and custodied at one of its oldest banks. This is not a cryptocurrency experiment. This is institutional plumbing.

USDC is natively issued on 32 blockchain networks and seamlessly moves between them, built on open protocols with a supporting suite of APIs and SDKs. Built specifically for 24/7 markets, USDC helps firms execute trades in real time, optimize capital, and reduce settlement risk, all with full-reserve backing and institutional transparency.

What makes Circle’s position in the tokenization ecosystem so powerful — and so strategically significant — is not just what USDC is. It is where USDC is. Expanding use of USDC in tokenized assets, prediction markets, AI-driven payments, and potential U.S. crypto legislation has strengthened the view that Circle’s core stablecoin infrastructure will see sustained demand. Roughly 98% of AI-agent payments are already settled in USDC. Visa now allows U.S. issuers and acquirers to settle transactions in USDC. Intuit has entered a multi-year partnership to embed USDC into its platform. Mastercard has welcomed Circle into its prestigious Crypto Partner Program. The company that most people outside of finance have never encountered is, in practical terms, becoming impossible to route around.

The U.S. government has notably opted for a private-sector-led model for the digital dollar, essentially outsourcing the “Digital Dollar” function to regulated players like Circle. USDC has become the preferred currency for purchasing and settling tokenized assets. In 2026, autonomous AI agents have begun performing micro-transactions, and these agents require a native internet currency that is programmable and settles instantly — USDC has become the de facto standard for this nascent economy.

has also demonstrated, in the most literal sense possible, that it practices what it preaches. Circle settled $68 million across its eight internal entities using USDC, circumventing banking rails with transfers completing in under 30 minutes, replacing bank wires that typically take one to three days to clear. When the company issuing the digital dollar starts using its own product to run its treasury operations instead of the traditional banking system, it is a reasonable signal that the product actually works.

CIRCLE AND THE NYSE: THE PARTNERSHIP THAT CHANGES EVERYTHING

The relationship between Circle and the New York Stock Exchange is perhaps the single most significant institutional development in the tokenization story — and it has received roughly one-tenth the coverage it deserves.

Circle and Intercontinental Exchange — the NYSE’s parent company — have entered into an agreement to explore stablecoin integration across ICE’s markets. “We believe Circle’s stablecoins and tokenized digital currencies can play a larger role in capital markets as digital currencies become more trusted by market participants as an acceptable equivalent to the U.S. Dollar. We are excited to explore the potential use cases for USDC and USYC across ICE’s markets.”

To understand why this matters, consider what ICE is. Intercontinental Exchange is not just the New York Stock Exchange. It owns the NYSE, several futures exchanges, bond trading platforms, mortgage technology infrastructure, and settlement systems that process trillions of dollars in transactions daily. When ICE says it wants to explore using USDC as a settlement currency across its markets, it is saying that the world’s most important financial exchange operator is considering building its tokenized trading future on Circle’s regulated digital dollar. That is not a pilot program. That is the foundation of the next financial system.

The NYSE is developing a platform for continuous trading and on-chain settlement of tokenized securities. The proposed platform will enable 24/7 operations including “instant settlement, orders sized in dollars, and stablecoin-based funding.” The announcement describes the initiative as a new NYSE venue that supports trading of tokenized shares fungible with traditionally issued securities as well as tokens natively issued as digital securities.

The phrase “stablecoin-based funding” in that announcement is doing an enormous amount of quiet work. There is currently one regulated stablecoin with the institutional relationships, the reserve backing, the regulatory approvals across multiple jurisdictions, and the explicit partnership agreement with ICE to serve that role. Its name is USDC, and it is issued by Circle.

CIRCLE AND POLYMARKET: THE PREDICTION MARKET PARTNERSHIP

If the NYSE relationship establishes Circle as the settlement layer for institutional tokenized finance, its partnership with Polymarket establishes it as the settlement layer for the disruptive new markets threatening to replace traditional finance’s most profitable intermediaries — starting with the sports betting industry’s beloved vig.

Circle has struck a partnership with Polymarket that will see the prediction marketplace shift to native USDC — redeemable one-to-one for U.S. dollars — for dollar-denominated settlement. The transition is intended to standardize dollar-denominated collateral across the platform, replacing bridged USDC with native USDC issued by Circle’s regulated affiliates.

The shift reduces dependency on bridge architecture while offering a settlement asset tied directly to Circle’s regulated reserves. Rather than treating all dollar-pegged tokens as interchangeable, platforms are beginning to differentiate based on issuance structure, compliance posture, and redemption guarantees. For prediction markets — where collateral stability directly affects pricing confidence — aligning with a regulated settlement asset influences how participants assess counterparty and platform risk.

Prediction markets such as Polymarket processed more than $22 billion in trading volume in 2025, largely using USDC as the settlement currency. As Polymarket grows — and it is growing at a rate that should unsettle every sportsbook executive on the planet — it grows on USDC rails. Circle doesn’t just benefit from that growth; Circle is structurally embedded in it.

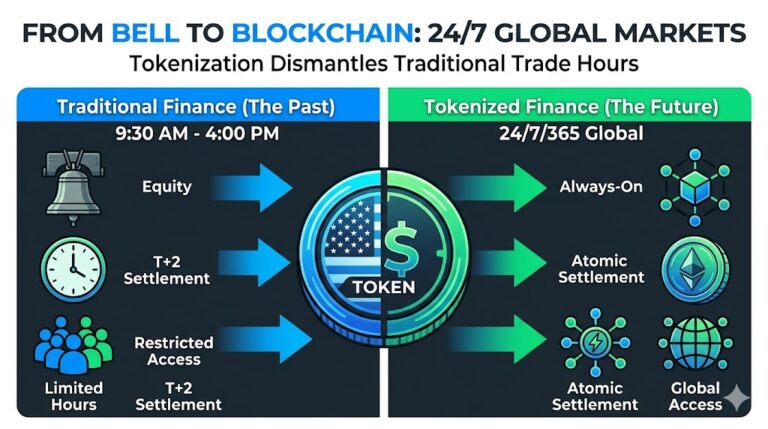

THE DEATH OF THE CLOSING BELL

For as long as modern finance has existed, the trading day has had hard edges. The New York Stock Exchange opens at 9:30 a.m. Eastern and closes at 4 p.m. It does not trade on weekends. It does not trade on federal holidays. A pension fund manager in Tokyo wanting to react to breaking news at 11 p.m. on a Friday can do precisely nothing until Monday morning — by which point the market has already moved, the opportunity is gone, and the moment has passed.

Robinhood CEO Vlad Tenev has framed this bluntly, arguing that the technology to enable constant trading is here and that its adoption is a matter of when, not if. “There was a time when you couldn’t trade stocks on your phone,” he wrote. “Imagine explaining to someone in 2035 that back in 2025, markets closed on weekends and holidays.” He has elsewhere described asset tokenization as an “unstoppable freight train” set to consume the entire global financial system. For a man running a brokerage company, that is either visionary candor or an unusually enthusiastic description of what is about to run him over. Probably both.

The mechanics are straightforward. In a fully tokenized ecosystem, trading windows no longer revolve around New York or London. Markets become continuously open, so investors anywhere in the world can buy or sell U.S. and global securities whenever local demand, news, or liquidity conditions make sense for them. Using smart contracts that automate clearing and settlement, on-chain tokenized trading can settle in seconds rather than the traditional T+1 delay — freeing up capital almost immediately rather than leaving it stranded in the clearing system overnight.

The settlement currency in that 24/7 world? USDC. USDC is built specifically for 24/7 markets, helping firms execute trades in real time and reduce settlement risk around the clock. When the NYSE’s tokenized trading platform goes live with stablecoin-based settlement, the stablecoin most likely to handle the clearing is the one its parent company has already struck an exploratory agreement with. The circle is closing — no pun intended.

Nasdaq has filed with the SEC to tokenize every listed stock, a move that would be the first time tokenized securities trade on a major U.S. exchange. Under the proposal, investors would be able to choose whether to settle trades in traditional form or in tokenized blockchain form.

The Depository Trust & Clearing Corporation has stated its ultimate ambition is to tokenize its entire $100 trillion asset catalog. “This is no longer driven by FOMO,” said its global head of digital assets. “It’s truly driven by real business cases, client demands.”

The total market capitalization of tokenized stocks grew more than 50 times in 2025, surging from less than $30 million in early 2025 to over $700 million by year end. According to Citigroup, tokenized securities could reach $4 to $5 trillion by 2030. Every dollar of that market needs a settlement currency. Circle intends to provide it.

THE PEOPLE WHO WERE ALWAYS LOCKED OUT

The standard pitch for tokenization focuses on efficiency: faster settlement, lower costs, 24/7 access. These are real benefits, and the financial industry loves them because they save billions in operational costs. But the more profound argument for tokenization is democratic, not operational. It is about who gets in.

Emerging markets make up nearly 60% of global GDP and 85% of the world’s population but lag dramatically in financial asset accumulation. In emerging markets, people tend to allocate their assets 50% to 70% in real estate, 20% to 30% in cash, and only 5% to 15% in equities or mutual funds. This is not because people in emerging markets lack the desire to invest in global capital markets. It is because the barriers — account minimums, currency controls, foreign exchange restrictions, limited brokerage access — have historically made it impossible for most of them to participate.

Tokenization removes those barriers. And USDC, available to anyone with an internet connection in over 185 countries through Circle Mint, is the on-ramp. A factory worker in Lagos, a teacher in Manila, a small business owner in São Paulo — all can, with a smartphone, own a fractional interest in a U.S. Treasury bond, an S&P 500 ETF, or a tokenized share of commercial real estate in downtown Miami. The asset classes that have generated wealth for the upper tier of the global economy for generations are, for the first time, genuinely accessible to everyone. The digital dollar that makes each transaction possible — the settlement rail, the collateral, the medium of exchange — is USDC.

POLYMARKET, PREDICTION MARKETS, AND THE SLOW DEATH OF THE BOOKIE’S JUICE

While Wall Street has been busy tokenizing stocks and bonds, a quieter revolution has been taking place in a market that Wall Street has historically ignored: sports betting. And the instrument of disruption is not a new sportsbook app. It is a prediction market — specifically, Polymarket — and it is about to make the traditional sports betting industry look like a business model designed to exploit its own customers. Because it largely is.

Here is how the traditional sports betting industry works. You want to bet on an NFL game. The sportsbook offers you -110 on both sides of the spread. This means you bet $110 to win $100. If two people take opposite sides of the same bet at -110, the book collects $220 and pays out $210 to the winner. The extra $10 — roughly 4.5% — is the vig, or the juice, or the house’s built-in margin on every transaction. On less liquid markets like player props or niche sports, that vig can balloon to 8%, 10%, or higher. A bettor placing 1,000 bets against a 5% vig faces a massive headwind that even skilled handicappers struggle to overcome over time.

There is more. Win consistently at a sportsbook for three to six months and your maximum bet drops from $5,000 to $50. Sportsbooks limit or outright ban winning players as standard industry practice. The industry that markets itself as entertainment is, structurally, a business that profits most when its customers lose and penalizes them when they don’t.

Polymarket operates on an entirely different model. Instead of placing a fixed-odds wager, you buy and sell shares tied to a specific outcome. Each contract trades between $0.00 and $1.00, where the price represents the market’s implied probability. Prices move based on supply and demand rather than a bookmaker’s internal model. There is no built-in vig.

Sports markets carry a taker fee of just 0.75% — a fraction of the margin embedded in traditional sportsbook odds. On Polymarket, prices come straight from the order book with no markup. The structural math is not close. On a $10,000 bankroll with a 55% win rate over 100 bets, Polymarket nets approximately $1,200 in profit while a traditional sportsbook nets roughly $400 for the same performance. The difference is entirely explained by the cost of the vig.

Now layer in Circle’s USDC. Every contract on Polymarket, every trade, every settlement, every payout — all of it runs on USDC. Since Polymarket processes crypto payments, it can issue payouts in a matter of hours, if not minutes, compared to traditional sportsbooks where bank transfer payouts can take days. That speed is not a feature of Polymarket’s design team. It is a feature of USDC’s settlement architecture. Circle built the rails. Polymarket is the train.

By 2026, Polymarket has processed more than $27 billion in total trades since its founding, and after acquiring a CFTC-licensed exchange and gaining full regulatory approval, the platform returned to the U.S. market in late 2025. The platform that was briefly exiled from America is now fully licensed and operating — and its partnership with Circle to transition to native USDC settlement means every dollar wagered on Polymarket is now settled through the most regulated, most institutionally trusted stablecoin in existence.

The 2026 FIFA World Cup, taking place this summer in the United States, Canada, and Mexico, is expected to be the moment Polymarket announces itself to the mass market. The platform currently hosts over 110 active markets for 2026 predictions, with its World Cup markets already drawing substantial volume. When hundreds of millions of soccer fans globally are looking for a place to put their convictions on the line during the biggest sporting event on the planet, a platform with no vig, instant USDC settlement, and global accessibility will make a very powerful impression on anyone who has ever been limited by a sportsbook for the crime of being too good at predicting outcomes.

The traditional sportsbook industry — built on geographic monopolies, state-by-state licensing, and a vig baked into every single transaction — is staring at a competitor that operates federally, settles in seconds, charges a fraction of the cost, and cannot ban winning players because there is no house to do the banning. This is what disruption looks like before most people notice it is happening.

OWNING THE EMPIRE STATE BUILDING FOR $500: REAL ESTATE AND ART TOKENIZATION

If prediction markets represent the disruption of one legacy industry, real estate tokenization represents the disruption of the oldest wealth-building vehicle in human history — and one that has been systematically unavailable to anyone without serious capital.

The premise is elegant in its simplicity. Take a $50 million commercial building in downtown Miami. Create a legal structure — typically a Special Purpose Vehicle — that holds the building. Issue 50,000 tokens, each representing a $1,000 ownership interest. Sell the tokens on a regulated platform. Token holders receive proportional rental income, distributed automatically via smart contract, and can sell their tokens on a secondary market whenever they choose. The settlement currency when tokens change hands? USDC.

While traditional real estate investments are rarely accessible with budgets under $100,000, blockchain real estate can be purchased for as little as $1,000. Commercial property tokenization moves all real estate deals to blockchain, simplifying access to cross-border objects and automating compliance checks and investor audits through smart contract logic.

In 2025, tokenized real estate assets surpassed $10 billion in value. Projections for 2026 forecast the market expanding to over $1.4 trillion, with institutional players like BlackRock and major pension funds increasing their allocations to tokenized real-world assets.

Circle has introduced tools for tokenizing real-world assets on the Arc blockchain — its open Layer-1 network optimized for internet-based commerce. Through Circle Contracts, developers can deploy pre-vetted smart contract templates for fungible tokens without needing to code in Solidity. In plain English: Circle is not just issuing the settlement currency for tokenized assets. It is building the blockchain infrastructure on which those assets are created, managed, and traded. It is the mint, the ledger, the settlement system, and increasingly, the exchange — all in one regulatory-compliant package.

The art world presents an equally dramatic opportunity. Tokenized art means new venues for investors and artists alike — artists and dealers find it easier to sell work to a larger and more diverse audience, and the public finds it easier to participate in one of the oldest, most prestigious marketplaces available. A Basquiat painting valued at $30 million could be tokenized into 30,000 fractional interests at $1,000 each, traded on a regulated platform, with dividend-equivalent distributions paid in USDC whenever the painting generates licensing revenue or appreciation events. The art world’s extraordinary returns, historically accruing only to wealthy collectors and institutional funds, become available to a nurse in Orlando or a small business owner in Jacksonville.

The same logic applies to every landmark asset historically locked behind a wall of capital requirements — and in every case, USDC functions as the settlement rail that makes fractional ownership liquid, global, and instant.

THE TOKENIZABLE UNIVERSE: AN INCOMPLETE AND DELIBERATELY AMBITIOUS LIST

The breadth of what can be tokenized is, at this point, limited primarily by imagination and regulatory clarity — and both of those barriers are falling fast. Here is a survey of asset classes currently being tokenized or with clear near-term potential:

Traditional Financial Assets: U.S. Treasury bonds and government securities are already the largest category of tokenized assets, with over $5.8 billion on-chain led by BlackRock’s BUIDL fund. Corporate bonds, money market funds, and private credit instruments are following rapidly. JPMorgan, Goldman Sachs, and BNY Mellon all have live tokenized money market products. Circle’s own USYC — a tokenized money market fund — already has $1.5 billion in assets under management.

Real Estate: Residential, commercial, industrial, and mixed-use properties. Single-family rental portfolios. Hotel and hospitality assets. Data center real estate. Farmland and agricultural land. A single property is placed into an SPV and its shares tokenized, with investors buying tokens representing fractional ownership later tradeable on regulated secondary markets. All rental income distributed automatically in USDC via smart contract.

Fine Art and Collectibles: Paintings, sculpture, photography, and digital art. Rare collectibles — vintage watches, classic automobiles, rare coins. Sports memorabilia. Rare comic books. First-edition manuscripts. Signed guitars. Championship rings. The first-edition Honus Wagner baseball card, currently owned by one person. Tokenized and fractionalized, it could have 50,000.

Luxury Assets: Jewelry companies and luxury goods manufacturers can make NFTs part of the ownership experience, introducing new opportunities for limited-run merchandise and tracking ownership and capturing a piece of resale prices. Wine and whisky cellars. Rare sneakers. Haute couture fashion. The 1962 Ferrari 250 GTO that recently sold for $51 million, fractionalized into 51,000 co-owners instead of one.

Intellectual Property and Royalties: Music royalties — the ongoing revenue streams from hit songs, catalogs, and publishing rights. Film and television royalty streams. Patent licensing revenue. Book royalties. Podcast advertising revenue. A songwriter could tokenize her entire catalog today, raising capital against future royalty streams while investors participate in the upside — with distributions settled daily in USDC.

Commodities: Tokenized gold, carbon credits, and oil are already active categories in the real-world asset space. Silver, platinum, and rare earth elements. Agricultural commodities — wheat, corn, soybeans — allowing farmers to hedge future harvests and investors to gain direct commodity exposure without futures contracts.

Infrastructure and Energy: Toll roads, bridges, airport terminals. Solar farms and wind energy installations. Energy storage facilities. Broadband infrastructure. Distributed ledger technology could deliver estimated annual global infrastructure operational cost savings of $15-20 billion.

Sports and Entertainment: Athlete investment tokens — shares in the future earnings of a professional athlete. Platforms have already let soccer clubs sell tokens allowing investors to earn a cut of player transfer fees. Franchise equity tokens. Concert venue tokens entitling holders to revenue sharing and priority access. Imagine owning a fractional interest in a first-round NFL draft pick, with a smart contract distributing his signing bonus proportionally in USDC.

Carbon Credits and ESG Assets: Verified carbon offset credits, biodiversity credits, ocean plastic credits, renewable energy certificates — all natural candidates for tokenization, creating transparent and liquid markets for environmental assets that currently trade in opaque over-the-counter markets.

Emerging and Creative Assets: Domain names and digital real estate. Private equity fund interests. Litigation finance — fractional interests in potential proceeds of pending lawsuits. Space infrastructure. The first hotel on the moon, when it eventually exists, will almost certainly be financed at least in part through tokenized fractional ownership, with construction draws settled in USDC.

THE INFRASTRUCTURE CHALLENGE: SPEED BUMPS ON THE WAY TO THE FUTURE

Candor requires acknowledging that the vision outlined above runs somewhat ahead of present reality. The tokenization revolution is real, the direction is clear, and the institutional commitment is genuine — but the technical infrastructure still has significant work ahead of it.

Current layer-1 blockchains suffer from three critical failures: a throughput ceiling where networks cannot handle the volume that real markets demand; latency issues where slow block times make efficient price discovery nearly impossible; and front-running by sophisticated bots that manipulate transaction ordering, undermining transparency and trust.

These are engineering problems, not conceptual ones. Circle’s Arc blockchain — its own Layer-1 network built specifically for institutional finance — is designed to address precisely these constraints. Arc is Circle’s open Layer-1 blockchain optimized for internet-based commerce, enabling institutions to bring custody, tokenization, and stablecoin payments into production with confidence. Circle is not waiting for someone else to build better infrastructure. It is building it.

Circle and Fireblocks have announced a strategic collaboration combining Circle’s stablecoin network with Fireblocks’ $10 trillion transaction infrastructure, enabling seamless stablecoin payments, settlement, custody, tokenization, and trading operations across the largest ecosystem of banks, payment providers, stablecoin issuers, exchanges and custodians. The ecosystem being assembled around USDC is not a collection of startups. It is a coalition of the most significant financial infrastructure companies in the world.

On the regulatory front, the passage of the GENIUS Act in 2025 established the first federal regulatory framework for stablecoins, reducing the volatility and uncertainty typically associated with digital currencies. The expected passage of the Clarity Act in 2026 is further opening the door to widespread tokenization. Circle spent years positioning itself as the “adult in the room” of the stablecoin industry — fully reserved, independently audited, regulatory-friendly. That positioning is now paying extraordinary dividends as regulation finally catches up with the technology.

THE BOTTOM LINE

The financial system being built through tokenization is not a marginal improvement on the existing one. It is a different system — more open, more accessible, faster, cheaper, and available to everyone regardless of their net worth, their geography, or their time zone.

At the center of that system, issuing the regulated digital dollar that settles every trade, backs every token, powers every prediction market contract, and moves through 32 blockchain networks in seconds rather than days, sits Circle Internet Group. It is the company that built the monetary infrastructure for the internet economy before most people realized that the internet economy needed monetary infrastructure. It is now listed on the New York Stock Exchange — the very institution it is partnering with to transform global capital markets — under the ticker CRCL.

Circle has successfully shed its image as a mere “crypto startup” to become a foundational pillar of global financial infrastructure. By bridging the gap between traditional fiat currencies and blockchain-based settlement, Circle is positioning USDC as the primary protocol for the “Internet of Value.”

The tokenization of everything is not coming. It is already here, in early form, growing at rates that make most technology adoption curves look gentle. The institutions that understand this are moving fast. The assets that used to require you to know the right people, live in the right city, or have the right net worth are becoming, one token at a time, available to everyone.

The market is open. It runs 24 hours a day, seven days a week, 365 days a year. The settlement currency is USDC. The closing bell is not part of the plan.

Florida Business Newsroom — Brandon, Florida — Finance, Technology & Markets

This article is for informational purposes only and does not constitute financial or investment advice. Tokenized assets, stablecoins, and prediction market contracts involve risk. Past performance does not guarantee future results. Consult a licensed financial advisor before making investment decisions. USDC and CRCL references are for informational context only and do not constitute an endorsement or investment recommendation.